We've got you covered

We are here to guide you in making tough decisions with your hard earned money. Drop us your details and we will reach you for a free one on one discussion with our experts.

Imagine you are required to hold both a short and long position on Nifty Futures simultaneously. Both positions would expire in the same series. What would you do?

In this chapter,We will discuss these questions. Let's first understand how it can be done. Then we will move on to why this is important (if you're curious, arbitrage might be the answer).

As you might have realized, options are versatile derivative instruments. You can use them to create any type of payoff structure, including futures (both short and long futures payoff).

This chapter will explain how options can be used to artificially duplicate a long-term payoff. Before we move on, it is worth reviewing the long Future's linear payoff.

Alternativ, you can also check out the quick overview at

The breakeven point is the time at which the long futures position was initiated. The futures will move higher than the breakeven points, and you lose money if they move lower below it. A 10 point move up will make you a profit, while a move down will make you lose. This linearity in payoff is why the future is sometimes called a linear instrument.

Synthetic Longs are designed to create a similar long Future with options.

It is easy to create a synthetic long.

This is why it's important to ensure that -

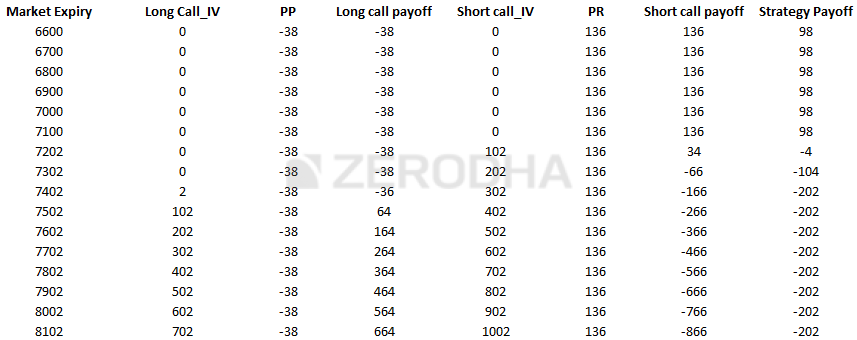

Let's take an example to better understand the situation. Let's say Nifty is at 7399. This would give 7400 ATM strike. Synthetic Long would mean we need to be long on 7400 CE. The premium is Rs.107. We would also have to short 7400 PE at 80.

The net cash flow would be the difference in the premiums (i.e. 107 -80 =).27.

Considering further few scenarios of market expiry-

Scenario 1: Market closes at 7200 (below ATM).

The 7400 CE would become worthless at 7200. We would also lose the premium, i.e. Rs.107/-. The 7400 PE would still have intrinsic value.let's calculate this below-

Intrinsic value for Put Option = Max [Strike Spot, 0]

Max [7400-7200, 0]

=Max [200, 0, 0]

= 200

We would be losing money on the premium that we have already received, as we don't have this option. It would result in a loss of -

80-200 = -120

The total payoff for the short Call and long Put positions would be -

= -107 -120

=-227

Scenario 2: Market closes at 7400 (At ATM).

Both options would be worthless if the market closes at 7400.

Note that 27 is the strategy's net cash outflow, which is the difference between the premiums.

Scenario 3: Market expires at 74227 (ATM + Difference Between the Two Premiums).

This is an interesting level. It is the breakeven point of the strategy. We don't make or lose any money at this point.

Scenario 4: Market closes at 7600 (above ATM).

The 7400 CE would be worth 200 at 7600. We would make -

Premium - Intrinsic Value

= 200 -107

= 93

We retain Rs.80 premium, so the 7400 PE would be worthless.

The strategy's total payoff would be -

= 93 +80

= 173

The above four scenarios show that the strategy is profitable when the market moves higher, and loses money when the market falls lower, much like futures. This does not mean that the payoff will be identical to futures. We need to evaluate the strategy's payoff in relation to the breakeven point. Let's say it is 200 points above or below that breakeven point. If the payoff is the same, it is clear that there is linearity in its payoff, which is similar to futures.

Let's get this out of the way.

This is the breakeven point.

ATM + Difference between the premiums

= 7400 + 27

=7427

This point should have a symmetric payoff. We will be considering7427 + 200 = 76227And7427-200 =7227This is how it works.

At 7627

At 7227

There is a payoff symmetry surrounding the breakeven.Synthetic Long is a simulated long that mimics the long-term payoff.

Here is the payoff at different expiry levels:

When we plot the Net Profitoff, we see a payoff structure that is very similar to long-call futures.

After we have figured out how to set-up a Synthetic long, it is time to determine the most common circumstances in which a synthetic long might be required.

Let's assume you are familiar with Arbitrage. Arbitrage can be described as the opportunity to purchase goods/assets in a cheaper market, and then sell them in more expensive markets. You get the profit. Arbitrage trades can be risk-free if executed correctly. Let me give you an example of an arbitrage opportunity.

Let's suppose you live near a city that has a lot of fresh fish. The rate at which fish can be sold in your area is low. A neighboring city, 125kms away, has a large demand for the same fresh seafish. The same fish can be purchased in the neighboring city for Rs.150 per Kg.

If you are able to purchase fish in your city for Rs.100, and then sell it in your neighboring city for Rs.150, you will get Rs.50. You will need to pay for transport and logistics. However, Rs.50 per Kg is still possible. It is still a great deal, and it is typical of arbitrage in the fish markets!

This looks great, but it's not risky.

It is risk-free and nothing will change. However, if the circumstances change, your profitability will also change. Let me tell you a few things that could happen.

I trust the above discussion has given you an overview of arbitrage. Any arbitrage opportunity can be described mathematically. Let's take the fish example as an example.

[Cost of selling fish to town B - Cost for buying fish in the town A] = 20

Arbitrage opportunities exist when there is an imbalance in any of the equations. Arbitrage opportunities exist in all markets, including the stock market, fish market, agrimarket, currency market and currency market. They are all governed using simple arithmetic equations.

Arbitrage opportunities are available in nearly every market. To spot them and make a profit, one must be an attentive observer of the market. Stock market-based arbitrage opportunities can allow you to lock down a small but guaranteed profit and keep it no matter what the market does. Arbitrage trades are a popular choice for risk-tolerant traders.

Here is a simple case of arbitrage that I'd like to talk about. Its roots lie in the idea of"Put Call Parity". I won't be discussing the Put Call Parity Theory, but will instead illustrate one of its applications.

This arbitrage equation is based on Put Call Parity.

Short Synthetic Long Futures + Long Synthetic Long Futures = 0

This can be further elaborated to:

Long ATM Call + Short AT Put + Short Futures = 0.

According to the equation, the P&L at expiry due to holding a long synthesized long and short future should equal zero.Well the Put call Parity is the answer to this.

If the P&L has a value other than zero, we have an opportunity to arbitrage.

To understand this let's take an example-

21 st January, the Nifty spot was at 7304 and Nifty Futures traded at 7316.

79.5 and 73.5 respectively traded the 7300 CE (ATM options) and 7300 PE (CE). All the contracts are from the January 2016 series.

If one executes the trade according to the above arbitrage equation, the positions will be -

Note that the first two positions form a long synthetic lengthy. As per the arbitrage equation, the positions should expire with a zero P&L.

Scenario 1 - Expiry at 7200

We are now experiencing a positive, non-zero P&L, rather than a 0 payoff.

Scenario 2 - Expiry at 7300

Scenario 3 - Expiry at 7400

This could be used to test the market for any expiry value, meaning that markets can move in any direction. However, you're likely to get 10.35 points.upon expiry.This is what I want to emphasize again: arbitrage allows you to make 10.35 upon expiry.

Below is the payoff structure for different expiry dates.

Isn't it intresting?you may think what's the catch?

Transaction fees

You must consider the cost of execution to determine if the trade is still worth it. This is how it works:

Considering these costs, it may not be a good idea to try to trade arbitrage for 10 points. It would make sense if the reward was higher, perhaps 15 or 20 points. You can maneuver the STT trap with 15 to 20 points. However, it will only shave off a few points.