We've got you covered

We are here to guide you in making tough decisions with your hard earned money. Drop us your details and we will reach you for a free one on one discussion with our experts.

We've covered multi-leg bullish strategies in the five previous chapters. These strategies can be used to suit a variety of market outlooks, from a bullish outlook to moderate bullish. You will have seen that professional options traders prefer to use spread strategies over taking on naked option positions. Spreads can reduce overall profitability but also give you greater insight into risk. Professional traders place more importance on 'risk visibility than profits. It's better to accept smaller profits than higher profits, provided you understand your maximum loss in the worst-case scenario.

Spreads are interesting because they almost always involve financing. This means that the purchase of one option is paid for by the sale or rent of another option. Spreads are distinguished from a naked directional position by financing. We will be discussing strategies that you can use when your outlook is from mildly bearish to very bearish in the following chapters. These strategies are similar to the bullish strategies we have discussed in the module.

We will begin with the Bear Put Spread. This is, as you might have guessed, the equivalent to the Bull Call Spread.

The Bear Put Spread works in the same way as the Bull Call Spread. A bear put spread would be used when the market outlook for the future is moderately bearish. This means that you expect the market will fall in the short term but not expect it to drop much. A 4-5% correction would be appropriate if I had to define moderately bearish. Invoking a bear spread would result in a modest profit if the market corrects (go down as expected), but if they do go up, it will result in a small loss.

A conservative trader, also known as a risk-averse trader, would use the Bear Put Spread strategy to simultaneously -

The Bear Put Spread does not have to be made with the OTM or ITM option. Any two options can be used to create the Bear Put Spread. The trade's aggressiveness will determine the strike choice. Both options must have the same expiry as the same underlying. Let's look at an example to better understand how the implementation works under different circumstances.

Nifty currently stands at 7485. This would translate into 7600 PE In the cash and 7400 PE out of the money. To sell 7400 PE in the 'Bear Put Spread, one would need to sell 7400. The premium from this sale would partially finance the purchase 7600 PE. Premium paid (PP), for 7600 PE, is Rs.165. The premium received (PR), for 7400 PE, is Rs.73/-. This transaction would result in a net debit of -

73-165

=-92

We will be looking at different situations to understand how the strategy's payoff works in different circumstances. Keep in mind that the payoff occurs upon expiry. This means that trader are expected to keep these positions until expiry.

Scenario 1- At 7800,Market expires (7600 i.e above the long put option)

This is an example where the market has gone higher than expected. Both the 7600 and 7400 put options, which have an intrinsic value of 7800, would be worthless at 7800.

Note that the '-ve sign associated to 165 means that there is money outflow, while the +ve sign associated with the number 73 indicates that money has been received into the account.

The net loss of 92 corresponds to the strategy's net debit.

Scenario 2- market closes at 7600(long put option)

This scenario assumes that the market will expire at 7600. We have bought a Put option.Later ,at 7600,both PE 7600 and 7400 will expire (similar to scenario 1) and this will cause a loss of 92

Scenario 3: Market closes at 7508 (breakeven).

7508 is halfway through 7600 and7400. I chose 7508 to show that the strategy doesn't make or lose any money at this point.

This would make 7508 the breakeven point in this strategy.

Scenario 4: Market expires at 7400 (at the short put option).

This is a very interesting level. Do you recall that when we first placed the position, the spot was at 74985. Now, the market has fallen as expected. Both options could have interesting outcomes at this point.

The strategy's net payoff is consistent with its overall expectations. That is, the trader makes a small profit when the market falls.

Scenario 5: Market expires at 7200 (below short put option).

This level is interesting because both options would have intrinsic value.Understand how the no. will add up-

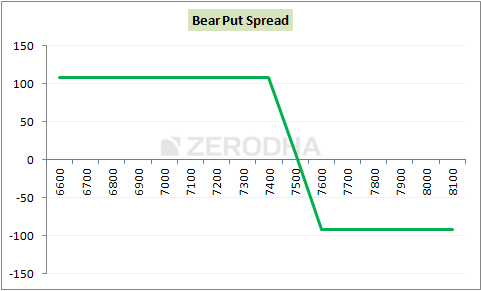

I've summarized all the scenarios (I've added the payoff values after taking into account the premiums).

| Market closes | 7600(long put) | 7400(short put) | Payoff(net) |

|---|---|---|---|

| 7800 | 0 | 0 | -92 |

| 7600 | 0 | 0 | -92 |

| 7508 | 92 | 0 | 0 |

| 7200 | 400 | 200 | +108 |

Note that the net return from the strategy is consistent with the strategy's overall expectation. This means that the trader makes a small profit when the market falls, while the losses are limited if the market rises.

Take a look at this table

Below is a table showing the strategy payoff for different expiry levels. When markets are up, the losses are limited to 92 and profits to 108.

We can draw some generalizations from the scenarios discussed above.

These are all important points that you can see in the strategy payoff chart.

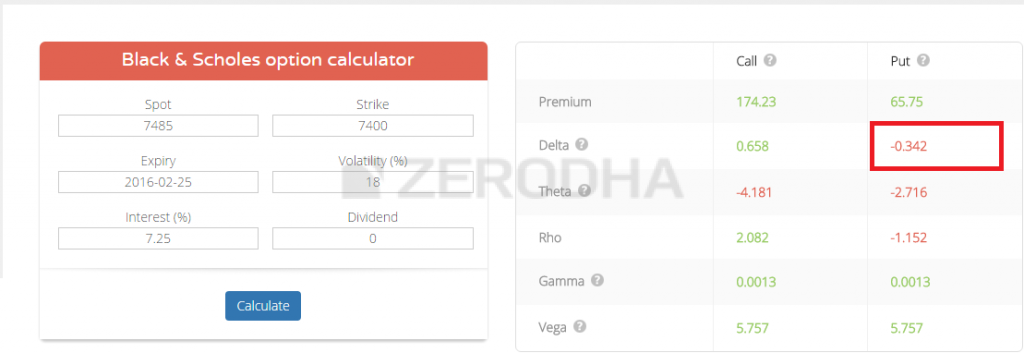

This is something I didn't mention in the previous chapters . However, it's better to be late than never . Always add up the deltas when you implement an option strategy. To calculate the deltas, I used the B & S calculator.

The delta of 7600 PE lies at -0.618

The delta of 7400PE is -0.342

The negative sign means that the premium for put options will decrease if markets rise, while premiums will increase if markets fall. However, the 7400 PE has been written, so the Delta would be.

-(-0.3422)

+ 0.342

Because deltas are additive, we can add the deltas together to get the combined delta for the position. It would be:

-0.618 + (+0.342).

= - 0.276

This indicates that the overall delta for the strategy is 0.276. if the market go down ,the premiums will go up,as the (-)ve implies. You can also add up the deltas for other strategies, such as Bull Call Spread, Call Ratio Back Spread etc. and you'll see that all of them have a positive Delta, which indicates that the strategy is bullish.

It can be difficult to determine the overall bias of a strategy if you have more than two options legs. In such cases, you can quickly add the deltas to find the bias. If the deltas are equal to zero, it is a sign that the strategy does not bias in any particular direction. These strategies are known as 'Delta Neutral'. These strategies will be discussed in the module's final point.

You may also be interested to learn that, while delta neutral strategies are immun to the market's directional movement, they react to fluctuations in time and hence are sometimes called "Volatility-based strategies".

A bear put spread's strike selection is very similar to a bull call spread's. I trust you are familiar with the 1st half' and 2nd halves of the series methodology. If you don't know what the '1st half of the series' and 2nd half of it, I suggest that you read section 2.3.

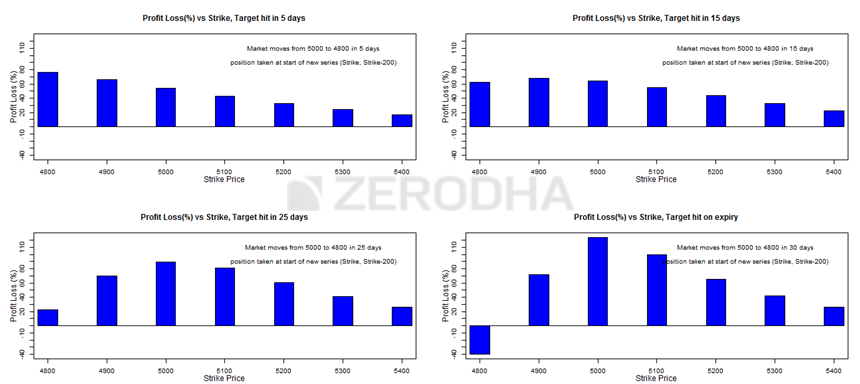

Take a look at this graph -

If you are in the first part of the series (ample amount of time to expiry), and the market is expected to fall by approximately 4%, then choose the following strikes to create spread

| 4% move to expected to happen within | strike(Higher) | strike(lower) | on graph |

|---|---|---|---|

| 5 days | Far OTM | Far OTM | Top left |

| 15 days | ATM | Slightly OTM | Top right |

| 25 days | ATM | OTM | Bottom left |

| At expiry | ATM | OTM | Bottom right |

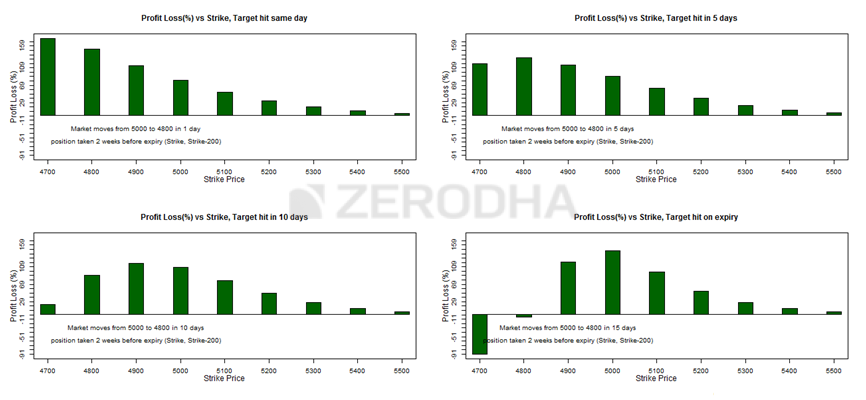

Assuming we are now in the 2 nd part of the series, it would make sense to select the following strikes for the spread.

| 4% move expected to happen within | strike(higher) | strike(lower) | on graph |

|---|---|---|---|

| Same day (even specific) | OTM | OTM | Top left |

| 5 days | ITM/OTM | OTM | Top right |

| 10 days | ITM/OTM | OTM | Bottom left |

| At expiry | ITM/OTM | OTM | Bottom right |

I hope that you find the following tables helpful in deciding which strikes to make for the bear spread.

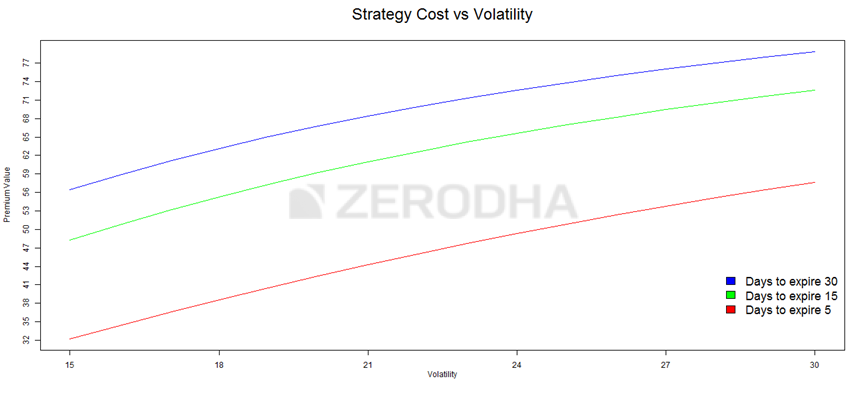

Now, we will shift our attention to the impact of volatility on bear put spread. Take a look at this image.

The graph below shows how the premium changes with time and volatility.

These graphs show that volatility changes should not be worrying when there is plenty of time for them to expire. The volatility should be considered between the midpoint and expiry. If volatility is expected increase, it is best to avoid taking the bear put spread.