We've got you covered

We are here to guide you in making tough decisions with your hard earned money. Drop us your details and we will reach you for a free one on one discussion with our experts.

In the previous chapter, we discussed "The net present value (NPV). The DCF valuation model plays a crucial role in NPV. Now that we have understood the concept, let's look at some related topics to DCF valuation model. These concepts will be further explored by us implementing the DCF model at Amara Raja Batteries Limited. (ARBL). This will bring us to the end of the 3 rd stage in Equity Research. The Valuation.

To evaluate the price of the pizza machine, we examined the future cash flows and then discounted them to obtain the present value. To calculate the NPV, we added all future cash flows and their present value. We also considered the possibility that the stock of the company could replace the pizza machine. We will price the stock based on the future cash flows of the company.

What cash flow is this? How can we predict the cash flow of a company's future?

The cash flow analysis for DCF is called the "Free Cash flow (FCF)." of the company. After accounting for capital expenditures like buying land, buildings and equipment, the free cash flow is the surplus operating cash the company generates. After accounting for capital expenditures, this is the cash that shareholders receive. How much cash the business can generate is what will ultimately determine its health.

This is also called free cash. It is the cash that the company has left after it has paid all expenses including investment.

Free cash flow is a sign that the company's health is good. Investors are attracted to companies that have rising or declining free cash flows, even though their share prices are low. They believe this will make the difference in the long-term, and the gap will diminish.

The company's free cash flow allows us to see if it has earned earnings over the past year. To assess the financial health of a company, investors should look at its free cash flow in addition to the earnings.

The cash flow statement can easily be used to calculate FCF for any company. This formula is:

FCF = Cash From Operating Activities - Capital Expensitures

Let's calculate the FCF of ARBL for the past 3 financial years.

| Particular | 2011 -12 | 2012 -13 | 2013 -14 |

|---|---|---|---|

| Cash from Operating Activities (after income tax) | Rs.296.28 Cars | Rs.335.46 | Rs.278.7 |

| Capital Expenditures | Rs.86.58 | Rs.72.47 | Rs.330.3 |

| Free Cash Flow (FCF) | Rs.209.7 | Rs.262.99 | (Rs.51.6) |

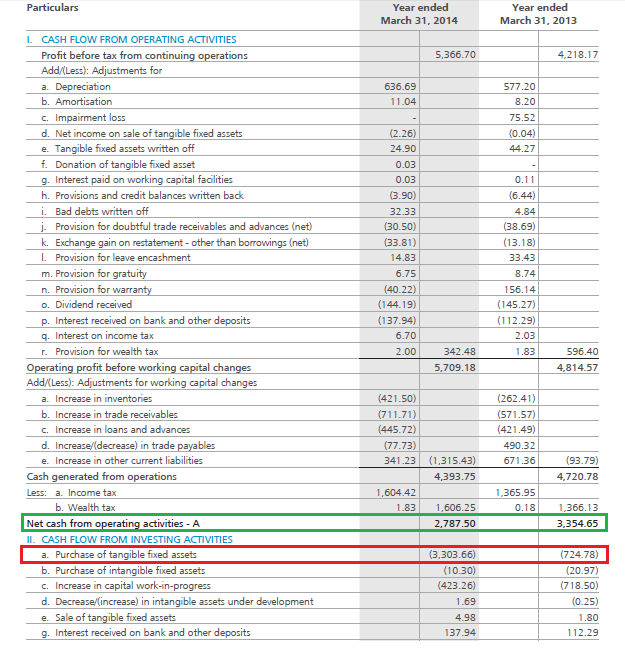

Here's a snapshot from ARBL's FY14 Annual Report. You can by yourself also calculate the free cashflow -

Note that the Net cash from operating activities has been adjusted for income tax. The capital expenditure is highlighted red, while the net cash from operating activities are highlighted in green.

Now you may be thinking about a point: If the goal is to calculate the future cash flow, then why do we still need to calculate the historical cash flow? It is easy to see why we are using the DCF model. We need to forecast the future free cash flow. It is possible to predict the future free liquidity by first estimating the historical free cash flow, then increasing the free cash flow at a specific rate. This is the industry standard.

The next question is how much growth can we expect and what about the free cash flow. The growth rate that you would expect should be conservative. Personally, I like to project the FCF for at most 10 years. This is done by increasing the cash flow at a specific rate for the first five years and then factoring in a lower rate over the next five years. For clarity, I recommend the following step-by-step calculation.

Step 1Calculate the average cash flow.

In the first step, I calculate the ARBL's average cash flow over the past 3 years.

= 209.7 + 262.99+ (51.6)

=Rs.140.36 Crs

To account for the business's cyclical nature, we take the average cash flow over the past 3 years. ARBL's latest cash flow for the year is negative at Rs.51.6 Crores. This is clearly not an accurate representation of ARBL cash flow. Therefore, it is always recommended to use the average free cash flow figures.

Step 2Identify the growth rate.

Choose a rate that you consider reasonable. This is the rate at the which cash flow will increase in the future. I prefer to grow my FCF in two stages. The 1st stage covers the first 5 years. The second nd phase covers the final five years. Concerning ARBL, I prefer to use around 18% for the first five years and 10% for the next five. If the company being considered is mature and has grown to a certain level (as in large-cap companies), I prefer a growth rate between 15% and 10%. This is where it's important to be conservative.

Step 3Calculate the future cash flows.

The average cash flow for 2013-14 is Rs. 140.26 Crs. With 18% growth, cash flow for 2014-2015 is expected to be -

= 140.36 * (1+18%).

= Rs. Rs.

The 2015-2016 free cash flow is estimated at -

165.62 * (1 +18%)

= Rs. Rs.

And so on. This table gives you the details of the calculation.

A future cash flow estimate -

| Sl No | Year | Growth rate assumed | Future Cash flow (INR Crs) |

|---|---|---|---|

| 01 | 2014 – 15 | 18% | 165.62 |

| 02 | 2015 – 16 | 18% | 195.43 |

| 03 | 2016 – 17 | 18% | 230.61 |

| 04 | 2017 – 18 | 18% | 272.12 |

| 05 | 2018 – 19 | 18% | 321.10 |

| 06 | 2019 – 20 | 10% | 353.21 |

| 07 | 2020 – 21 | 10% | 388.53 |

| 08 | 2021 – 22 | 10% | 427.38 |

| 09 | 2022 – 23 | 10% | 470.11 |

| 10 | 2023 – 24 | 10% | 517.12 |

This gives us a good estimate of future cash flow. These numbers are not reliable, but you might be wondering. Predicting the free cash flow requires predicting sales, expenses, and virtually every aspect of the business. The future cash flow estimate is just that, an estimate. It is important to be conservative while still assuming a free cash flow growth rate. For the future, we have assumed a growth rate of 18% to 10%; these numbers are conservative for a well-managed and growing company.

For up to 10 years, we have attempted to predict the future cash flow. What would happen to the company if it was no longer profitable after the 10 th years? Is it possible for the company to cease existence? It would not. It is not expected that a company will be a "going concern" that exists forever. This means that there will always be some cash generated as long as the company is still around. As companies age, however, the amount of free cash generated decreases.

The "The rate at which free cash flow increases beyond 10 years (from 2024 onwards) has been called the "The Rate of Free Cash Flow Growth".Terminal Growth Rate". The terminal growth rate is usually less than 5%. Personally, I prefer to keep this rate between 3-4 percent and not higher.

The"Terminal Value"The sum of all future cash flows beyond the 10ThYear, also known as the terminal year. We can calculate the terminal value by simply taking the cash flow for the 10ThYear and increase it at the terminal rate. The formula for doing this is however different because we are literally calculating the value to infinity.

Terminal Value = FCF multiplied by (1 + terminal growth rate) divided by (Discount rate - terminal growth rate).

The FCF used for the calculation of the terminal value is the FCF from the 10 th years. Let's calculate ARBL's terminal value using a terminal growth rate 3.5% and a discount rate 9%.

= 517.12 *(1+3.5%) / (9 - 3.5%)

=Rs.9731.25 Crs

We know the future cash flow over the next 10 years and the terminal value, which is the future cash flow of ARBL after the 10 th year. Now we need to calculate the cash flow value in today's terms. This is called the present value calculation. We will then add the present value to calculate the ARBL's net present value (NPV).

We will accept a discount rate of 9%.

ARBL will receive Rs.195.29 crore in 2015-16 (2 years from now). The present value would be - at a 9% discount rate

= 195.29/ (1+9%).2

= Rs.164.37 Crores

Here's how future cash flows will stack up in the present value.

| Sl No | Year | Growth rate | Future Cash flow (INR Crs) | Present Value (INR Crs) |

|---|---|---|---|---|

| 1 | 2014 – 15 | 18% | 165.62 | 151.94 |

| 2 | 2015 – 16 | 18% | 195.29 | 164.37 |

| 3 | 2016 – 17 | 18% | 230.45 | 177.94 |

| 4 | 2017 – 18 | 18% | 271.93 | 192.72 |

| 5 | 2018 – 19 | 18% | 320.88 | 208.63 |

| 6 | 2019 – 20 | 10% | 352.96 | 210.54 |

| 7 | 2020 – 21 | 10% | 388.26 | 212.48 |

| 8 | 2021 – 22 | 10% | 427.09 | 214.43 |

| 9 | 2022 – 23 | 10% | 470.11 | 216.55 |

| 10 | 2023 – 24 | 10% | 517.12 | 218.54 |

| Net Present Value (NPV) of future free cash flows | Rs.1968.14 Crs | |||

We also need to calculate net present value for terminal value. This is simply done by reducing the terminal value using a discount rate.

= 9731.25/ (1+9%),10

= Rs.4110.69 Crore

The sum of the current cash flows equals = NPV future cash flows + PV terminal value

= 1968.14 + 4110.69

= Rs.6078.83 Crores

This is how you stand today and look into the future. I expect ARBL will generate a completely free cash flow of Rs.6078.83 crores. All of this would be owned by ARBL shareholders.

Now, we are at the final step in the DCF analysis. Based on future cash flow, we will calculate ARBL's share price.

Now we know how much ARBL will likely generate in free cash flow. We also know how many shares are currently outstanding on the markets. The ARBL per-share price is calculated by dividing the total cash flow by the number of shares.

Before doing this, however, we must calculate the value of "Net Debt" from the balance sheet. Net debt is the total amount of current-year debt less current-year cash & cash balance.

Net Debt =

Current Year Total Debt plus Cash & Cash Balance (C&CB)

ARBL would calculate this based on the FY14 Balance Sheet.

Net Debt = 75.94-294.5

= (Rs.218.6 Cros)

Negative signs indicate that the company has less cash than it owes. This must be added to the present value of all cash flows.

= Rs.6078.83 Crores - (Rs. = Rs.6078.83 Crs - (Rs.

= Rs.6297.43 Crores

Divide the above numbers by the number of shares to get the share price of the company, also known as the intrinsic value of a company.

Share price = Total Present Value of Free cash flow/ Total number of shares

ARBL's annual reports show that there are 17.081 crores of outstanding shares. The intrinsic value, or per-share value, is therefore -

= Rs.6297.43 Crs/ 17.081 Crs

Shares starting at Rs.368

This is in fact the final output from the DCF model.

Although the DCF model is quite scientific, it relies on many assumptions. It is an art form to make assumptions in finance. As you gain experience and progress, you become better at making assumptions. We should therefore assume (yet again) that we made some mistakes in calculating the intrinsic value for all practical purposes. We should therefore allow for modeling errors.

Leeway for modelling errors allows us to be flexible in calculating per-share values. For what I consider the stock's intrinsic worth, I prefer + 10% for the upper band and -5% for the lower band.

That is how we calculate -

Lower intrinsic value = 368 * (between 10% and 15%) = Rs. 331

Higher intrinsic value = Rs.405

Instead of taking Rs.368 as the stock’s fair value, I would assume that the stock is reasonably valued between 331 to 405. This would be the intrinsic price band.

We now consider the stock's market value. We conclude the following based on the stock's current market price:

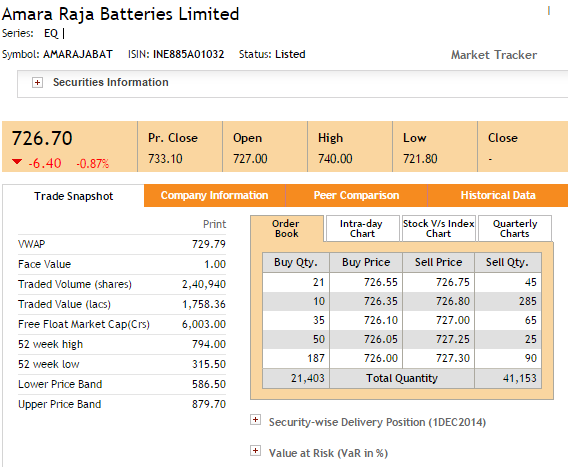

These guidelines are the basis for checking Amara Raja Batteries Limited stock price today (2 and Dec 2014.). Here's a snapshot taken from the NSE website.

The stock trades at Rs.726.70 per share! The stock is trading at Rs.726.70 per share! This is a clear indication that one would not buy the stock at such high valuations.

Activities surrounding long-term investing and long-term investment are slow-moving locomotive trains. On the other hand active trading is like a fast bullet train. The market will linger for a while when there is long-term value. It doesn't disappear quickly. We now know that Amara Raja Batteries Limited's current market price is too high. It trades at a level that is way above the upper limit for the intrinsic value band. The scene was completely different one year ago. Based on FY 2013-2014, ARBL's intrinsic values band is Rs. 331 to Rs.405.

Here's the ARBL chart -

The blue highlight shows that the stock traded within the band for nearly 5 months. The stock could have been purchased at any time during the year. You didn't have to move once you bought the stock. The returns would roll in your favor if you stayed put!

This is why they say that bear markets create value. The markets were bearish throughout 2013, creating valuable buying opportunities for quality stocks.

We have covered different aspects of equity risk research in the three chapters that preceded this one. Equity research, as you might have guessed, is the process of looking at the company from three perspectives (stages).

We focused on the qualitative aspects of company in stage 1. This stage focuses on the qualitative aspects of the company. This is a crucial stage in equity research. If I don't feel convinced, I stop researching further. Markets are full of opportunities. Don't force yourself into a situation that doesn't suit you.

Only after I have been 100% satisfied with the findings of stage 1, I move on to stage 2. Stage 2 is basically where we apply the standard checklist and evaluate the company's performance. This is my version of what I consider a good checklist. You are asked to create your own checklist because that would be helpful. However, you should ensure that you use reasonable logic when including each item.

If the company passes both stages 1 and 2, I move on to equity research stage 3. Stage 3 is where we compare the stock's market value with its intrinsic value. The stock that trades at a lower price than its intrinsic value is considered a good investment. It isn't, however.

If all three stages are completed to your satisfaction, then you will be able to buy the stock. You can buy the stock once you are satisfied with the process.