We've got you covered

We are here to guide you in making tough decisions with your hard earned money. Drop us your details and we will reach you for a free one on one discussion with our experts.

Now we know that the Delta value of an option is a variable. It changes with the value in the underlying. Let me repost this graph showing the delta's movements

(image 1).

The blue line that represents the delta of a call options is very clear. It can be seen from the top, where it crosses between 0 to 1, or possibly 1 to 0, depending on the circumstances. Similar observations can be made regarding the red line representing the delta of a call option. The value does not change from 0 to 1. This graph reinforces the fact that the delta is an variable that changes continuously. This is why one must ask "What's the delta?"

As I am reasonably certain that the answer to the first question is obvious as we move through this chapter, we will first discuss the 2 nd questions.

The Gamma, also known as curvature of option, is the rate at which an option's delta changes with the underlying. Gamma is often expressed as deltas lost or gained per one-point change of the underpinning. The delta increases by the amount the gamma when it rises, and falls by the amount the gamma whenever it falls.

Consider this example:

Let's get this figured out.

The 8400 CE premium went up from Rs.26 and Rs.47 to cover Nifty's move from 8326 to8396. Along with that, the Delta rose from 0.3 to 0.4575.

The option changes from OTM option to ATM option with the 70 point change. This means that the option's delta must change from 0.3 up to somewhere around 0.5.Same thing we see here.

Let's assume that Nifty rises 70 points over 8396. We will see what happens to the 8400 CE option.

Let's go a step further. Assume Nifty drops by 50 points. Now let's see what happens to the 8400 CE option.

You will be amazed at how smoothly the delta follows the rules for determining the delta value. You may also wonder why the Gamma values are kept constant in these examples. In reality, Gamma changes with changes in the underlying. The changes in the underlying cause a change in Gamma. This is captured by three rd derivatives of underlying, called "Speed" (or "Gamma Of Gamma") or " Dgamma spot". It is not necessary to discuss Speed unless you are mathematically inclined, or if you work in an Investment Bank, where there can be a lot of trading book risk.

The Gamma, unlike the delta is always positive for both Call Option and Put Option. When a trader has both Calls and Places options, he is called 'Long Gamma.' If he has only short options (both calls or puts), he's called 'Short Gamma.

Consider this example: If the underlying moves by 10 points, the Gamma for an ATM Put option equals 0.004, what would the new delta be?

Before you move on, I suggest that you take a moment to consider the following.

The solution is simple: Since we are discussing an ATM Put option the Delta must be approximately -0.5. Remember that put options have a ve Delta. Gamma is, as you can see, a positive number. +0.004. +0.004.

Case 1: Underlying moves up 10 points

Case 2: Underlying decreases by 10 points

Here's the trick question: In the previous chapters, it was mentioned that the Delta of the Futures agreements is always 1. So, what do you think the Gamma of the Futures agreements is? Leave your comments below with your answers.

13.2 - Use of Gamma for estimating risk

Many traders set their trading risk limits. This is what I mean when I say "risk limit". A trader might have Rs.300,000. Each Nifty Futures contract requires a margin of Rs.16,000. To calculate the margin for any F&O contract, Stock market box's calculator can be used. The trader can decide to limit his holdings of 5 Nifty futures at any time. This will define his risk limits and is fair and efficient while trading futures.

However, does this logic apply to trading options? Let's see if this is the best way to view risk when trading options.

This is an example of a situation:

The trader has 10 lots of Nifty 8400 call option; this indicates that he is within his risk limit. Remember the Delta chapter discussion about adding up the delta. To get the total delta for the position, we can simply add the deltas. Each delta of 1 is 1 lot of the sub-underlying. This will help us to keep things in perspective and allow us to calculate the delta of the overall position.

The overall delta perspective shows that the trader is within his limit of trading no more than 5 Futures lots. Do not forget that the trader has limited options and is short gamma.

The position's delta value of 5 means that trader's position will move by 5 points for every 1 in the underlying.

Let's say Nifty moves 70 against him. The trader will continue to hold his position hoping for a recovery. He is clearly under the impression that he has 10 options, which is within his risk appetite.

Let's look at the forensics and see what is happening behind closed doors.

Can you see the problem? The trader, who had set a 5 lot risk limit, has now increased his exposure to 8.5 lots. This is way more than his perceived risk limit. Unexperienced traders can be unaware of this and believe that they are well within their risk radar. In reality, his risk exposure increases.

His overall position should move by 8.5 points for every 1 point change in the underlying, since his delta is 8.5. Let's suppose that the trader is now long on the option call rather than short. This is a positive situation, as the market is moving in his favour. The positive market movements are making his positions 'Longer. The deltas tend to grow with the 'long Gamma. The delta tends grow which means that the premium rate to change the underlying tends be faster.

If you find it confusing, suggest you read it again in smaller pieces.

The trader is actually short gamma. This means that if the position moves against him (as when the market moves up while the trader's short), the deltas add up (thanks gamma). Therefore, at every stage in market growth, the deltas and gamma conspire against the short option trader making his position more risky than what the naked eye can see. This is why shorting options can be a risky business. You can even say that shorting options are at risk of being short gamma.

Not to be confused with the previous statement, I am not suggesting you should avoid shorting options. A successful trader will use both short and longer positions depending on the circumstances. I am merely pointing out that you should be aware of the Greeks when shorting options and what they can do for your positions.

Additionally, I strongly recommend that you refrain from shorting option contracts with a high Gamma.

This brings us to another topic: what is considered large gamma?

We briefly discussed earlier in this chapter that Gamma changes refer to the change in the underpinning. The 3 rd ordered derivative called "Speed" captures this change in Gamma. For reasons I have already stated, I won't go into detail about 'Speed'. We need to understand the Gamma movement's behaviour so we don't trade with high Gamma. There are many other benefits to knowing how Gamma behaves, which we will discuss in a later stage of this module. We will now examine how Gamma reacts to changes in the underlying.

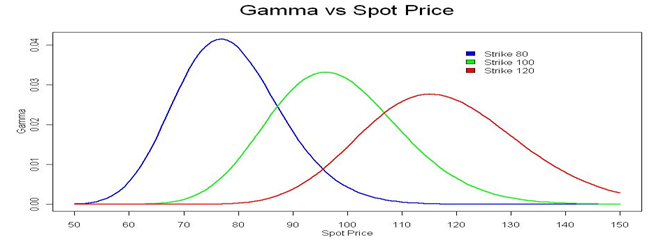

Take a look at this chart.

(IMAGe 2)

The chart below shows 3 different CE strike prices: 80, 100, 120, and their Gamma movements. The blue line is the Gamma for the 80 CE strike price. To avoid confusion, I suggest that you examine each graph separately. For simplicity sake, I will only be referring to the 80 CE strike option (represented by the blue line).

Let's assume that the spot price is 80 and the ATM strike 80. This will allow us to see the following chart.

In case the above discussion seemed overwhelming, here are three simple points you can take away.

Understanding how individual option Greeks react to different circumstances is key to options trading success. Understanding the individual Greek behavior is important, but it's also important to understand how individual Greeks interact with one another.

We have so far only considered the premium change relative to changes in spot price. Time and volatility are not topics we have yet to discuss. Consider the market and the real-time fluctuations that occur. All things change - volatility, time and the underlying prices. An options trader must be able to comprehend these changes and their overall impact on the option premium.

This is only possible if you are able to understand the inter interactions between the option Greeks. Examples of cross interactions between Greeks would include gamma and time, volatility and volatility, time versus delta, time vs. time, etc.

The final step in understanding the Greeks boils to a few key decision-making factors like -

Once you have a good understanding of individual Greeks and their inter-relationships, the answers to these questions will be clear.

This is how the module will be developed further.

As you can see, there are miles to go before we finally fall asleep

{kind=link}