We've got you covered

We are here to guide you in making tough decisions with your hard earned money. Drop us your details and we will reach you for a free one on one discussion with our experts.

The Bear call spread & the bear put spread are alike. It is a two-leg option strategy that is invoked when the market view is moderately bearish. In terms of payoff structure, the Bear Call Spread is very similar to the Bear Put Spread. However, there are some differences in strike selection and strategy execution. Bear Call Spread is a spread that uses 'Call options' instead of 'Put options', as in the bear put spread.

This stage may pose a fundamental question: Why should one choose a Bear Call spread instead of a Bear Put spread when they have similar payoffs?

This all depends on how attractive premiums are. The Bear Put spread can be executed with a debit while the Bear Call spread can be executed with a credit. If you're at a market point where -

If you are moderately bearish about the future, it is a good idea to invoke a Bear Call Spread to get a net credit instead of a Bear Put Spread to get a debit. Personally, I prefer strategies that offer net credit to strategies which offer a net debit.

The Bear Call Spread, a traditional two-leg spread strategy that uses OTM Call options and ITM Call options, is the Bear Call Spread. You can also create the spread with other strikes. Remember that the spread (difference) between the selected strikes is a sign of profit potential.

To apply the bear call spread, -

Assure -

Let's take an example to better understand it.

Date: February 2016,

Outlook - Moderately bearish

Nifty Spot – 7222

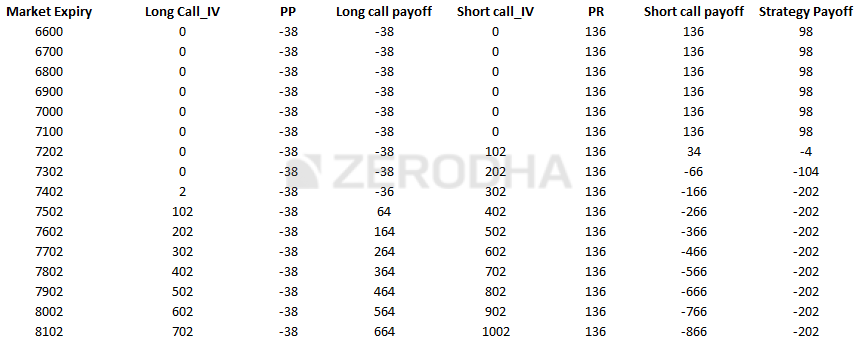

Trade setup for Bear Call Spread

A bear call spread generally has a net credit. This is why it is sometimes called a credit spread. The market can move in any direction after we have initiated the trade and it can expire at any level. Let's look at a few scenarios in order to see what the bear spread would do for different levels.

Scenario 1: Market expires at 7500 (above long Call).

Both the Call options would be worth 7500 and would therefore expire in the money.

Scenario 2: Market closes at 7400 (at long call).

The 7100 CE would lose its intrinsic value at 7400 and would therefore be worthless. The 7400 CE would be worthless.

Note that the 7400 loss is the same as the 7500 loss. This is due to the fact the maximum loss above a certain point is 202.

Scenario 3: Market closes at 7198 (breakeven).

The trade is not profitable or loss-making at 7198. This is called a breakeven point. Let's see how this plays out.

This shows that 7198 is not a profitable strategy.

Scenario 4: Market closes at 7100 (at a short call).

Both the Call options would cease to be worthless at 7100.

The strategy is profitable as long as the market falls.

Scenario 5: Market expires at 7 000 (below the short-call)

This scenario shows how profitable the strategy is in the event that the market falls further. Both call options would be worthless at 7000. We will keep the 7400 CE premium, which is Rs. 38, as a loss. However, the 7100 CE premium (which is Rs.136) will be retained as a profit. The net profit of the strategy would therefore be 136-38 =98The strategy is clearly profitable when the market falls. However, it has a limit of Rs.98.

Here's the payoff at different expiries.

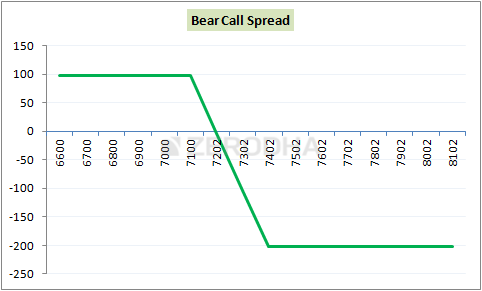

You can plot these payoffs to see the graph of strategy payoff.

In terms of of payoff, it's quite similar to the bear put spread where the scenario is predefined i.e . profit under best and losses under worst case.

The key trigger points of the strategy can be derived from the payoff.

We can now add the Deltas together to calculate the overall delta for the strategy's sensitivity.

The following Delta values were derived from the BS calculator:

The strategy's delta is negative. It indicates that the strategy loses money when the underpinning goes up and makes money when it goes down.

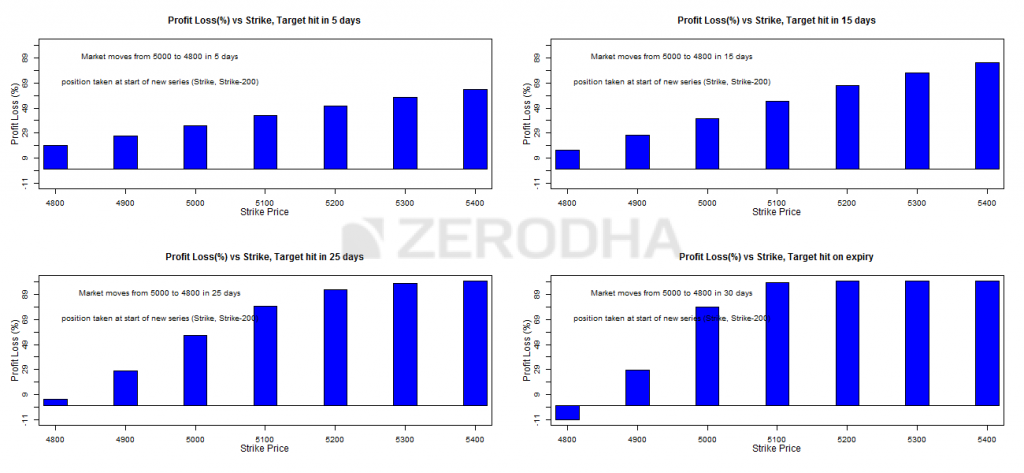

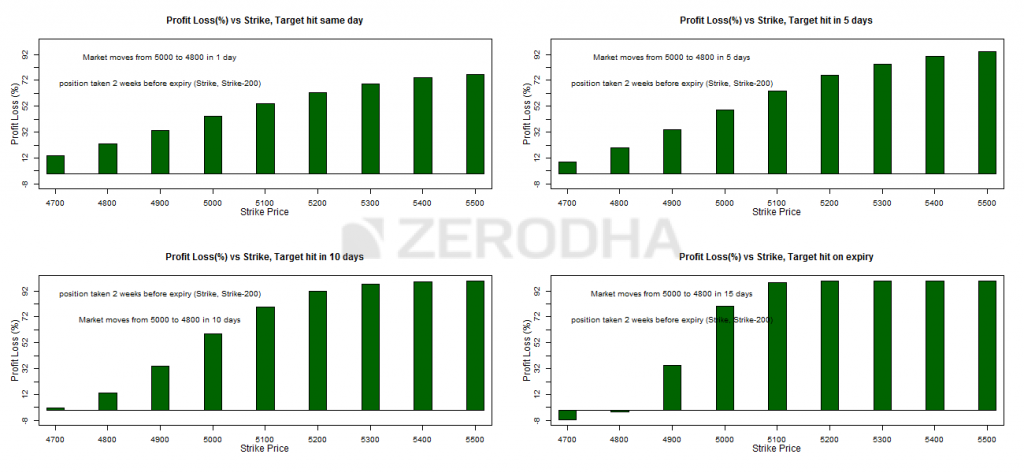

These images will help us determine the best call option strike, given the expiry date. The split of the time frame (1st and second half of the series) has been discussed many times before. I will only post the graphs as well as the summary table.

Strikes to choose when we're in the 1 st halves of the series .

.

| 4% move expected to happen within | strike(higher) | strike(lower) | on graph |

|---|---|---|---|

| 5 days | Far OTM | ATM+2 strikes | Top to left |

| 15 days | Far OTM | ATM + 2 strikes | Top to right |

| 25 days | OTM | ATM + 1 strike | Bottom to left |

| At expiry | OTM | ATM | Bottom to right |

Strikes to choose when we are in 2 nd the half of the series

| 4% move expected to happen within | strike(higher) | strike(lower) | on graph |

|---|---|---|---|

| 5 days | Far OTM | Far OTM | Top to left |

| 15 days | Far OTM | Slightly OTM | Top to right |

| 25 days | Slightly OTM | ATM | Bottom to left |

| At expiry | OTM | ATM/ITM | Bottom to right |

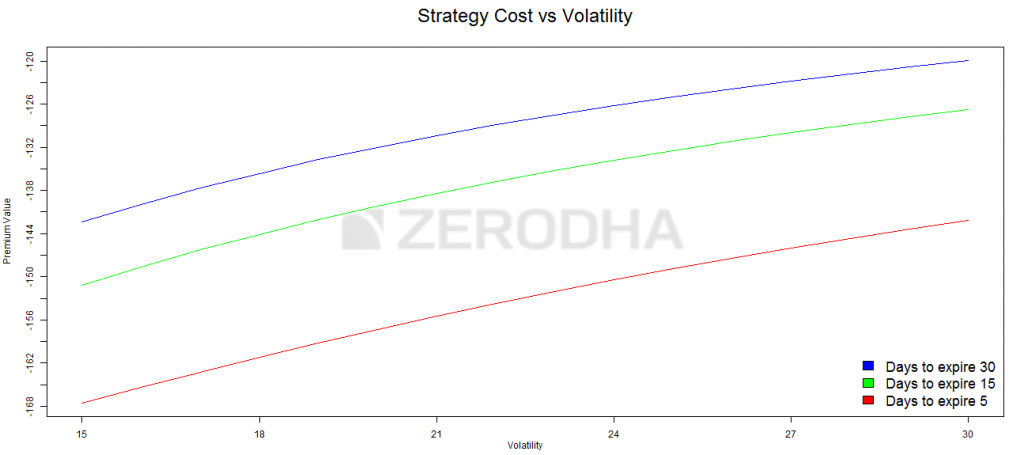

The graph below shows the variation in strategy costs with respect to volatility changes.

The graph below shows how the premium changes with time and volatility.

These graphs show that volatility changes should not be worrying when there is plenty of time for them to expire. The volatility should be considered between the midpoint and the end of each series. If volatility is expected to rise, it is best to avoid taking the bear call spread.